the General Administration of Customs (GAC) first implemented rules of expropriation and classification in 2013, and required that import duty on royalties shall be paid before importation of goods. Although the GAC created a new mechanism that allowed post-clearance payment in 2019, it has continuously strengthened supervision on the taxation of royalties due to the recent surging volume of royalty payments by foreign-invested companies in China.

Senior Partner

AllBright Law Offices

Consequently, many enterprises are not only required to repay tremendous amounts of overdue taxes, but also face the imposition of severe administrative punishment. To avoid financial and operational risks, it is essential that enterprises enhance their compliance with relevant rules and regulations.

Conditions of taxation

Under PRC laws and regulations, there are two necessary conditions of customs taxation of royalties. The first is royalty payments’ relevance to imported goods under rules of expropriation and classification. Enterprises should reasonably determine whether royalties are relevant to the imported goods by analyzing the actual circumstances of transactions in conjunction with categories specified by the rules.

The second condition is the royalty payment’s function as a precondition to the sale of the imported goods, meaning that the importer cannot purchase the goods, or use the goods in future production under conditions stipulated in the contract, without the royalty payment. Normally, customs bases its inspection procedures on both the content of contracts and documents indicating the nature of transactions.

Some exceptions

Although the two conditions of customs taxation of royalties appear clearly defined in relevant rules and provisions, their interpretation can be complicated by certain exceptional circumstances. One such circumstance is when royalty payment is made for duplication rights in China. For instance, if company A imports sample music albums from company B to duplicate and sell them in China, the duplication fee paid by company A doesn’t need to be declared to customs authorities.

Another circumstance is when the payment is made for technical assistance or management that doesn’t involve transfer of technology or licence. For example, if a Chinese company A imports manufacturing equipment from company B, which provides technical assistance for its manufacturing process, company A doesn’t need to declare the technical assistance fees to customs because they are incurred during manufacturing processes in China, and are only related to finished products.

Calculation method

Enterprises can follow three steps to calculate royalty taxes. The first step is to determine the amount of dutiable royalties by using the formula: Total dutiable royalties = total amount of royalty payment × percentage of the company’s value of imported goods out of total accrued base value of goods. If companies A and B each pay RMB10 million in royalties overseas, but the value of their imported goods counts for 20% and 60% of the total accrued base value, respectively, the dutiable royalties of companies A and B should be RMB2 million and RMB6 million.

The second step is to determine the royalty paid for each type of imported good. If company A imports goods X and Y (each counts for 10% of accrued base value) and company B only imports good Z, then the royalties paid for goods X, Y and Z should be RMB1 million, RMB1 million and RMB6 million, respectively.

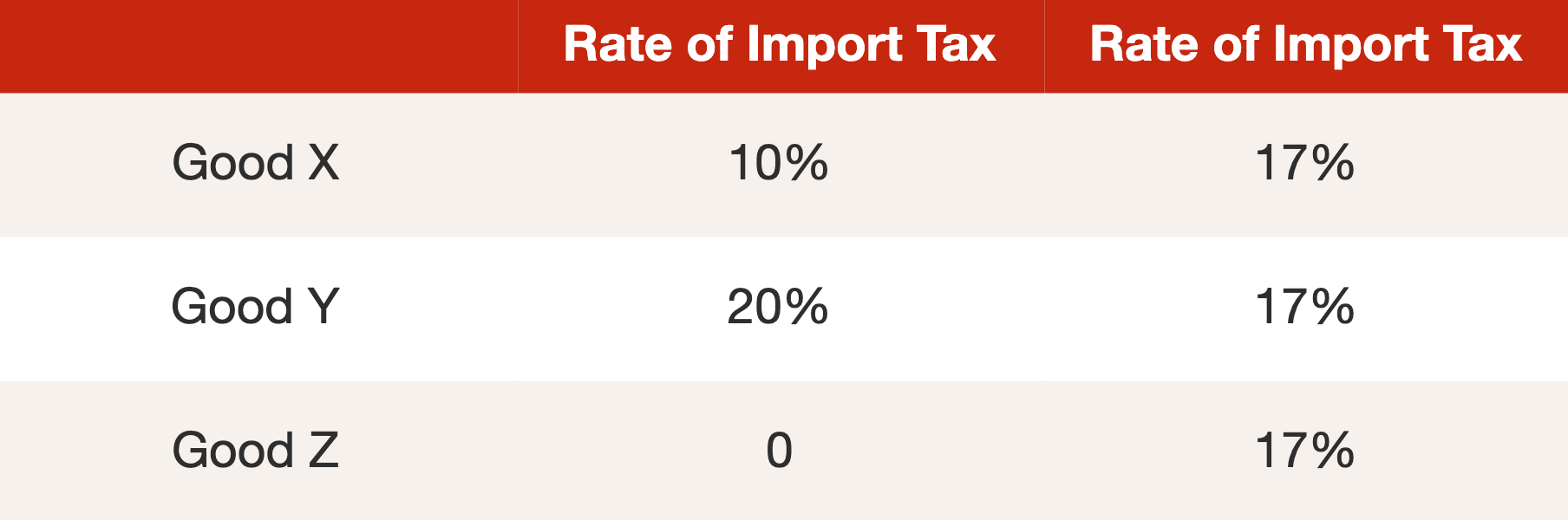

The third step is to calculate the amount of customs taxes. Suppose such rates of goods X, Y and Z are set as follows:

The composite tax rates of goods X, Y and Z should be 28.7%, 40.4% and 17% (composite tax rate = rate of import tax + rate of VAT + rate of import tax × rate of VAT), and the customs royalty tax for each good is calculated by multiplying the composite tax rate with royalties paid for the good. Accordingly, the customs tax for goods X, Y and Z is RMB287,000, RMB404,000, and RMB1.02 million. Thus, while companies A and B are both paying RMB10 million in royalties, the customs taxes paid are different in amount.

Three suggestions

The authors suggest that enterprises comply with the rules of customs taxation of royalties by taking the following measures:

Enterprises need to reasonably determine the nature of each royalty payment. To do so, enterprises should analyze the conditions stipulated in the trade agreements and the royalty agreements, in conjunction with evidence such as invoices, technical documents and materials, and financial reports to examine the nature of each royalty payment.

Enterprises should also properly separate royalty payments and avoid overpaying taxes for royalties that either don’t directly relate to the imported goods or don’t constitute preconditions to the sale of imported goods to China. Enterprises should provide evidence indicating the independent relationship between royalty payments and importation of goods including separate contracts with different parties for royalty payment and importation, financial records proving that transactions are completed without royalty payments, and invoices indicating importation of goods from a third party.

Enterprises are encouraged to communicate with customs authorities, offer evidence for their calculation, and explain the logic and reasons behind their decisions. This will prepare enterprises for possible disagreements raised by customs, and help them avoid fines and punishment.

Carl Li is a senior partner at AllBright Law Offices. Vera Zhao, a JD candidate from Stanford Law School, also contributed to this article

AllBright Law Offices

11/F and 12/F, Shanghai Tower

No. 501 Yincheng Middle Road

Pudong New Area, Shanghai 200120, China

Contact details:

Tel: +86 21 2051 1000

Fax: +86 21 2051 1999

Email: